Author: Eve Pope, Technology Analyst at IDTechEx

Carbon capture, utilization, and storage (CCUS) technologies strip carbon dioxide (CO2) from waste gases and directly from the atmosphere before either storing it underground or using it for a range of industrial applications. IDTechEx forecasts significant growth for CCUS. With approximately 50 megatonnes of CO2 captured annually by CCUS projects today, IDTechEx predicts this capacity will reach 2,500 megatonnes per annum by 2045. However, the rate of CCUS adoption will vary across industrial sectors.

According to IDTechEx’s report, “Carbon Capture, Utilization, and Storage (CCUS) Markets 2025-2045: Technologies, Market Forecasts, and Players”, early opportunities will be strongly linked to sectors with lower capture costs or the ability to generate additional revenue streams. Financial viability is the biggest barrier to CCUS project development, rather than technological maturity. Governments across the world have started introducing mechanisms to overcome this barrier.

In the European Union, an emissions trading scheme (ETS) attaches a price to every tonne of carbon dioxide. The idea is to make emitting CO2 more expensive than employing decarbonizing operations for industrial players. In 2023, the average ETS auction price was US$90/tonne of CO2. The US has opted for the carrot over the stick approach, offering tax credits (called 45Q) for CO2 that is captured and then utilized/sequestered – worth US$85/tonne of CO2. Many other countries, including China, have also introduced some form of carbon pricing, although the price attached to CO2 tends to be lower.

Even beyond these government interventions, corporations are voluntarily going further to reduce emissions. Voluntary carbon credit markets exist, with purchases of durable carbon removals skyrocketing in 2023 due to the high permanence and lack of reversibility associated with these credits.

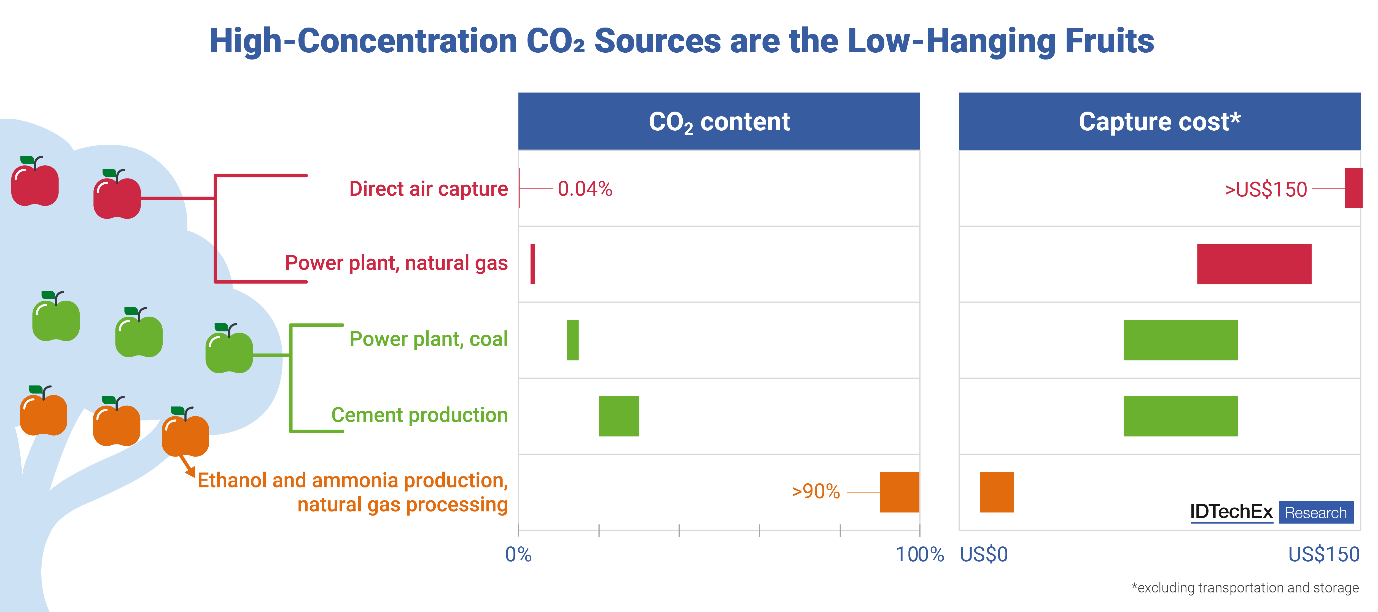

High concentration sources of CO2 are low-hanging fruit

The higher the concentration of CO2 in the flue gas stream, the less expensive it is to capture. This is because, at higher CO2 concentrations, systems must gather smaller quantities of air to capture the same amount of CO2, requiring smaller equipment and less energy. The lower the capture cost, the greater the financial benefit from CCUS.

Flue gas CO2 concentration and associated capture cost for various industrial sectors. Full capture cost analysis is available in the new IDTechEx CCUS report. Source: IDTechEx

Although CCUS costs are highly project-specific, government mechanisms such as the EU ETS and the US 45Q tax credit can, in general, comfortably cover the costs of capturing, transporting, and storing carbon dioxide from sectors such as natural gas processing and ammonia and ethanol production. In fact, natural gas processing dominates the CCUS landscape as of today, accounting for 65% of all carbon dioxide captured in 2023.

For CO2 captured from ethanol production, further opportunities exist. This is because most ethanol is produced by the fermentation of sugar from plants such as corn, barley, or sugar cane. Carbon dioxide originating from plants is classed as “biogenic”.

Industrial biogenic CCUS projects can generate revenue from carbon removal credits

Industrial sources of biogenic carbon dioxide include combustion of biomass to generate heat and power (bioenergy), production of ethanol, energy generation from waste with a biogenic fraction (waste-to-energy), pulp and paper production, and making biogas. As plants regrow, they take in atmospheric CO2 via photosynthesis, making the process of capturing and storing biogenic CO2 carbon negative over the timespan of a plant’s life. In contrast, fossil fuels take millions of years to reform once combusted.

Because permanently sequestering captured biogenic CO2 corresponds to durable, highly verifiable removal of carbon dioxide from the atmosphere, lucrative carbon removal credits can be sold on the voluntary carbon market. Such BECCS (bioenergy with carbon capture and storage) credits saw a breakout year for sales in 2023, led by Microsoft’s deal with Ørsted, with Microsoft purchasing 2.67 million tonnes of future removals from the Asnæs Bioenergy Power Station. BECCS credits sold for around US$300/tonne of CO2 in 2023 in voluntarily markets, easily covering CO2 capture, transportation, and storage costs for most BECCS projects. When IDTechEx attended the UK-focused sustainability conference, Innovation Zero 2024, three players intended to incorporate sales of BECCS credits into their business models: Drax (bioenergy), enfinium (waste-to-energy), and Future Biogas (biogas).

Outlook

CCUS is expected to play a crucial role in decarbonizing many sectors beyond the early opportunities listed here, including cement, fossil-fuel power generation, and blue hydrogen. There is also regional variation in CCUS project development. The US will continue to dominate CCUS over the coming decade, with the 45Q tax credit scheme providing a strong financial incentive for carbon capture.

To find out more about IDTechEx’s report, “Carbon Capture, Utilization, and Storage (CCUS) Markets 2025-2045: Technologies, Market Forecasts, and Players”, including downloadable sample pages, please visit www.IDTechEx.com/CCUS.

For the full portfolio of energy and decarbonization market research from IDTechEx, please see www.IDTechEx.com/Research/Energy.